As of January 31, 2020 at 09:50PM, 1 BTC equals 9372.75 USD.

Register PIVOT to get BTC Bonus:PIVOT is a community for cryptocurrency investors.

via free bitcoin

The internet giant, which some lawmakers and regulators say has grown too powerful, tweaked the way it displayed ads on search results. It did not go over well.

more @ New York Times

China's economy is grinding to a halt as the government scrambles to stop the spread of the deadly Wuhan coronavirus, fueling fears that efforts to contain the outbreak will have worldwide economic consequences.

Sixteen cities in China, with a combined population of more than 50 million people, are on lockdown. Airlines around the world are canceling flights to China and countries including the United States are urging residents not to travel to the country at all. Chinese companies began to shut down last week for the annual Lunar New Year holiday, but at a time when they would normally be preparing to get back to work, 14 provinces and cities, which account for more than two-thirds of China's economic output, announced that businesses may not resume operations for another week—at least.

China was already under economic pressure before authorities first reported cases of an unknown pneumonia to the World Health Organization in late December. Facing tensions from the trade war and sluggish demand at home, its official GDP growth in 2019 was the slowest since 1990. Now China, and the rest of the world, is preparing for the economic pain that seems likely to come with the epidemic.

"China's economy is very important in the global economy now, and when China's economy slows down we do feel that," said U.S. Federal Reserve Chairman Jerome Powell earlier this week. "Not as much though as countries that are near China, or that trade more actively with China, like some of the Western European countries."

The world's most populous nation has become integral to nearly every sector of the global economy. It is the world's largest manufacturer and imports more crude oil than any other country. Chinese travelers are the top spenders in international tourism, making 150 million overseas trips worth $277 billion in 2018. And the country's 1.3 billion population provides the largest market in the world for several categories of consumer goods—automobiles, spirits, luxury goods—according to the McKinsey Global Institute.

China's influence on the global economy is apparent in the brand names that are responding to the outbreak. General Motors and Honda, which manufacture vehicles in Wuhan, announced that they are trying to determine when to reopen. Apple is restricting employee travel and on Jan. 28 set an unusually wide range for its expected 2020 first-quarter earnings, citing "uncertainty" around the virus' impact. The CEO of Royal Dutch Shell called the outbreak a "concerning development" and said the oil giant is preparing for a "tough and uncertain" economic environment. The co-working company WeWork has temporarily shut more than 50 offices across China, and Facebook has stopped non-essential travel to the country. IKEA has shuttered all of its mainland China stores and KFC and Pizza Hut have closed thousands of branches. Starbucks has closed about half of its 4,100 shops in the mainland and McDonald's has temporarily shuttered stores across five cities in Hubei province, where Wuhan is located. Disney has closed its theme parks in Shanghai and Hong Kong.

Much bigger than SARS

The outbreak of the virus, which has sickened nearly 10,000, killed more than 200 in China, and spread to at least 20 countries, has evoked memories of another epidemic: severe acute respiratory syndrome (SARS), which started in China in 2002 and killed almost 800 people across the world. The economic impact of SARS was felt mostly in China. One study estimates that the SARS crisis cut the gross domestic product of mainland China by 1.1% and that of Hong Kong, where the services sector is a pillar of the economy, by 2.6%.

But since 2003, China has climbed from the world's sixth largest economy—just bigger than Italy—to the second largest, worth nearly $14.55 trillion in 2019, almost as large as the entire European Union. China is also an integral trading partner for the biggest economies the world. The U.S., Japan and India import more goods from China than anywhere else and the E.U. and Brazil sell more to China than to any other country. Experts say that's likely to mean any fallout from the Wuhan coronavirus outbreak will hit the global economy a lot harder than SARS did.

"The spillover will be much bigger, because China has a much bigger role in the world economy," Warwick McKibbin, an economist at Australian National University, and one of the authors on the study of the economic impact of SARS, tells TIME. "The incomes of a lot of Chinese have risen, there's a very large middle class and so the expenditure on travel and consumption of luxury type goods—that'll potentially be impacted in a totally differently than it was in 2003."

Financial markets have whipsawed this week as traders struggle to price in the risk of the outbreak. Investors have moved their money to safe havens like the U.S. dollar, the Japanese yen and gold. The prices of some commodities, including oil, have declined sharply over concerns that the virus and measures to contain it will lead to lower demand from China, according to Rabobank, a Dutch bank and financial services firm.

Industries bracing for hit as virus spreads

The Wuhan coronavirus appears less deadly than SARS, which killed almost 10% of those it infected, but infection numbers continue to surge. The fear of contagion could dampen consumer demand and impact everything from tourism to travel to trade and services in affected countries, according to Moody's Investor Services.

Fear is spreading fast. In Hong Kong, 900 miles from Wuhan, some of the only spots where large crowds could be seen gathering this week were outside of the city's pharmacies, where residents stood in line for hours or even camped out overnight to get their hands on new supplies of protective face masks when they hit the shelves. More than 700 miles from Wuhan in northwest Gansu province's capital city Lanzhou, normally bustling restaurants and bars in sit vacant. Streets in megacities like Beijing and Shanghai are nearly empty. In southwestern Yunnan province, almost every shop in the tourist destination of Lijiang was closed on Thursday—including four out of five pharmacies and a local clinic.

"Everyone here is terrified, the old city is in lockdown, nobody is leaving their houses," one restaurant owner in Lijiang tells TIME, asking to remain anonymous due to the sensitivity of the situation.

It is already apparent that the Wuhan coronavirus will hit tourism hard. Chinese authorities have announced a temporary ban on outbound group travel. Hong Kong, Taiwan, Singapore and the Philippines have stopped accepting visitors from China's Hubei province, and Russia and Mongolia have closed their borders with China. Airlines across the world, from United Airlines to British Airways have cut flights to and from China or suspended them altogether.

Thailand—a popular destination for Chinese tourists—expects to see two million fewer visitors from China over the next three months. In Japan, some tour companies have already had tens of thousands of cancellations. The chief economist at SMBC Nikko Securities estimates that if the Chinese government banned travel overseas for six months—an extreme scenario—spending by Chinese group tourists would decline $83.1 billion and take 0.1 percentage point off global economic growth.

"Key sectors, such as tourism, have become increasingly reliant on business from China," Mark Humphery-Jenner, an associate professor of finance at the University of New South Wales, tells TIME. "Coronavirus and its impact show that China is an important part of the world economy."

Production for sectors from automobiles to technology is also likely to take a hit. Several automakers have assembly plants in Wuhan, including General Motors and Honda. Toyota Motor Corp. has halted its China production until Feb. 9 and Apple's CEO, Tim Cook, said the company is taking steps to "make up any expected production loss."

McKibbin says that a lot has changed since 2003 and that today many companies are dependent on Chinese production. "It's actually hurting production chains."

Eswar Prasad, an economics professor at Cornell University, tells TIME that the outbreak may cause multinational companies that were already reassessing their supply chains, due to rising wages in China and trade war tensions, to reduce their production footprints in the country. He also sounds a stark warning.

"China's economy is now a global behemoth compared to its more modest size at the time of the SARS epidemic," he says, "so a shock to China's growth will have major reverberations across the world."

—With reporting by Charlie Campbell in Shanghai

The White House couldn't persuade Boris Johnson to keep Huawei out of Britain's 5G network.

more @ New York Times

Crude oil supply disruptions—realized or expected—can have large and immediate effects on crude oil prices. Two recent events, the September 2019 attacks on Saudi Aramco facilities at Abqaiq and Khurais (which disrupted crude oil volumes) and the January 2020 military operations in Iraq (which did not disrupt crude oil volumes), led to relatively large daily price changes and intraday price movements—movements within single trading days. Intraday prices of front-month Brent crude oil futures for the two events followed a broadly similar path at first: an upward movement as market participants reacted to the news and a downward movement as new information was incorporated.

read more

(SAN FRANCISCO) — A House subcommittee is investigating popular dating services such as Tinder and Bumble for allegedly allowing minors and sex offenders to use their services.

Bumble, Grindr, The Meet Group and the Match Group, which owns such popular services as Tinder, Match.com and OkCupid, are the current targets of the investigation by the U.S. House Oversight and Reform subcommittee on economic and consumer policy.

In separate letters Thursday to the companies, the subcommittee is seeking information on users' ages, procedures for verifying ages, and any complaints about assaults, rape or the use of the services by minors. It is also asking for the services' privacy policies and details on what users see when they review and agree to the policies.

Although the minimum age for using internet services is typically 13 in the U.S., dating services generally require users to be at least 18 because of concerns about sexual predators.

"Our concern about the underage use of dating apps is heightened by reports that many popular free dating apps permit registered sex offenders to use them, while the paid versions of these same apps screen out registered sex offenders," Rep. Raja Krishnamoorthi, the Illinois Democrat who heads the subcommittee, said in a statement. "Protection from sexual predators should not be a luxury confined to paying customers."

Match Group said it uses "every tool possible" to keep minors and bad actors off its services and continues to invest in technology to keep users safe. In an emailed statement, the company said the problem was broader and requires other parties, including app stores that know who their users are, "to do their part as well."

Match added that the national sex offender registry needs to be updated so that perpetrators' digital footprints can be tracked and blocked by social media and dating services.

Grindr and The Meet Group did not immediately respond to messages for comment on Thursday. Bumble did not have an immediate comment.

Besides safety issues, the investigation also seeks to address concerns about data the services request to make matches. Such information may include sexual orientation, gender identity, political views, and drug, alcohol and tobacco use.

The subcommittee cited a report by a Norwegian consumer group this month that found that dating apps including Grindr, OkCupid and Tinder leak personal information to advertising tech companies in possible violation of European data privacy laws. The Norwegian Consumer Council said it found "serious privacy infringements" in its analysis of how shadowy online ad companies track and profile smartphone users.

Match Group parent company IAC has said it shares information with third parties only when it is "deemed necessary to operate its platform" with third party apps. The company said it considers the practice in line with all European and U.S. regulations.

The internet giant posted increases in revenue and profit after shoppers flocked to it during the holiday season.

more @ New York Times

Arvind Krishna, who has led the company's cloud computing business, was named the new chief executive.

more @ New York Times

Amy Resnik touches the Space Shuttle Challenger Memorial after a wreath laying ceremony as part of NASA's Day of Remembrance, Thursday, Jan. 30, 2020, at Arlington National Cemetery.

January 30, 2020

Astronaut and station commander Luca Parmitano is tethered to the International Space Station while finalizing thermal repairs on the AMS.

January 29, 2020

As of January 30, 2020 at 09:50PM, 1 BTC equals 9390.8701 USD.

Register PIVOT to get BTC Bonus:PIVOT is a community for cryptocurrency investors.

via free bitcoin

Add a gun that can't shoot straight to the problems that dog Lockheed Martin Corp.'s $428 billion F-35 program, including more than 800 software flaws.

The 25mm gun on Air Force models of the Joint Strike Fighter has "unacceptable" accuracy in hitting ground targets and is mounted in housing that's cracking, the Pentagon's test office said in its latest assessment of the costliest U.S. weapons system.

The annual assessment by Robert Behler, the Defense Department's director of operational test and evaluation, doesn't disclose any major new failings in the plane's flying capabilities. But it flags a long list of issues that his office said should be resolved — including 13 described as Category 1 "must-fix" items that affect safety or combat capability — before the F-35's upcoming $22 billion Block 4 phase.

The number of software deficiencies totaled 873 as of November, according to the report obtained by Bloomberg News in advance of its release as soon as Friday. That's down from 917 in September 2018, when the jet entered the intense combat testing required before full production, including 15 Category 1 items. What was to be a year of testing has now been extended another year until at least October.

"Although the program office is working to fix deficiencies, new discoveries are still being made, resulting in only a minor decrease in the overall number" and leaving "many significant'' ones to address, the assessment said.

Cybersecurity 'Vulnerabilities'

In addition, the test office said cybersecurity "vulnerabilities" that it identified in previous reports haven't been resolved. The report also cites issues with reliability, aircraft availability and maintenance systems.

The assessment doesn't deal with findings that are emerging in the current round of combat testing, which will include 64 exercises in a high-fidelity simulator designed to replicate the most challenging Russian, Chinese, North Korean and Iranian air defenses.

Despite the incomplete testing and unresolved flaws, Congress continues to accelerate F-35 purchases, adding 11 to the Pentagon's request in 2016 and in 2017, 20 in fiscal 2018, 15 last year and 20 this year. The F-35 continues to attract new international customers such as Poland and Singapore. Japan is the biggest foreign customer, followed by Australia and the U.K.

By late September, 490 F-35s had been delivered and will require extensive retrofitting. The testing office said those planes were equipped with six different versions of software, with another on the way by the time that about 1,000 planes will be in the hands of the U.S. and foreign militaries.

A spokesmen for the Pentagon's F-35 program office had no immediate comment on the testing office's report.

Brett Ashworth, a spokesman for Bethesda, Maryland-based Lockheed, said that "although we have not seen the report, the F-35 continues to mature and is the most lethal, survivable and connected fighter in the world." He said "reliability continues to improve, with the global fleet averaging greater than 65% mission capable rates and operational units consistently performing near 75%."

The Mattis Test

Still, the testing office said "no significant portion" of the U.S.'s F-35 fleet "was able to achieve and sustain" a September 2019 goal mandated by then-Defense Secretary Jim Mattis: that the aircraft be capable 80% of the time needed to perform at least one type of combat mission. That target is known as the "Mission Capable" rate.

"However, individual units were able to achieve the 80% target for short periods during deployed operations," the report said. All the aircraft models lagged "by a large margin" behind the more demanding goal of "Full Mission Capability."

The Air Force's F-35 model had the best rate at being fully mission capable, while the Navy's fleet "suffered from a particularly poor" rate, the test office said. The Marine Corps version was "roughly midway" between the other two.

The Air Force and Navy versions are also continuing to have cracks in structural components, according to the report, saying, "The effect on F-35 service life and the need for additional inspection requirements are still being determined."

Gun Woes

The three F-35 models are all equipped with 25mm guns. The Navy and Marine versions are mounted externally and have acceptable accuracy. But the Air Force model's gun is mounted inside the plane, and the test office "considers the accuracy, as installed, unacceptable" due to "misalignments" in the gun's mount that didn't meet specifications.

The mounts are also cracking, forcing the Air Force to restrict the gun's use. The program office has "made progress with changes to gun installation" to improve accuracy but they haven't been tested yet, according to the report.

For years, climate activists have warned that a warming planet would bring devastation, disrupting not only developing countries and coastal communities but also the foundations of the global economy. Still, investors continue to pump billions of dollars into fossil fuels, governments prioritize policies to keep cheap oil flowing, and developers build on land that scientists say will soon be underwater.

Kristalina Georgieva, 66, the environmental economist who took the helm as managing director of the International Monetary Fund in October, has spent much of her career studying the problem. Now, she says, a slew of climate-related disasters have finally awakened the financial sector and the economic leaders who guide it. "The tide is turning," she told TIME in a Jan. 23 interview at the annual meeting of the World Economic Forum in Davos, Switzerland.

Georgieva plans to take advantage of this moment. The new chief of the IMF described a range of measures the global financial institution will take to prioritize climate change during her five-year term: supporting policies that require investors to disclose climate vulnerability, measuring a country's financial situation in part by its preparation for climate change, pushing countries around the globe to implement a carbon tax. "We have to create the right policy environment that is based on sound economics," she says. "I'm prioritizing this for the Fund."

At a time when much of the climate conversation centers on flashy policy prescriptions like the Green New Deal proposed by congressional Democrats, the climate policy of the IMF and the changing tune of the financial sector may sound wonky. But the climate challenge is unlikely to be met without the financial sector–and the authorities that regulate and govern it–on the right side of the fight. For decades, banks have given fossil-fuel companies the financing to mine and drill; meanwhile, governments have provided seemingly bottomless subsidies, some $5 trillion annually, the IMF said last year. At the same time, banks have largely ignored the risk that climate change poses to their customers, from businesses in the flood zone to homes in fire-prone areas.

At Davos, there were hints this may be changing. Just a few days before the conference, BlackRock, the world's largest asset manager, said climate change would lead to a "fundamental reshaping of finance" and promised to rethink its strategy. Microsoft pledged to go carbon-negative in a decade and remove by 2050 a sum of carbon equivalent to all that the company has ever emitted. The value of assets under management in the Net-Zero Asset Owner Alliance, a group of investors committed to having a zero-emissions portfolio by 2050, grew to more than $4.3 trillion. And the IMF warned that climate change "already endangers health and economic outcomes."

"I don't want to be naive, but I want to acknowledge that the center of the global economy is now saying things that many of us have dreamed they might for a long time," former Vice President Al Gore said at a dinner at Davos convened by WWF. "They're saying them forcefully and eloquently."

Two broad climate risks dominated the discussion among corporate executives and investors in Davos: physical risk and so-called transition risk. The former is obvious. Climate change drives extreme weather events and disasters, from flooding and drought to wildfires and heat waves, which can destroy infrastructure and devastate economies. IMF data shows that even seven years after a devastating tropical storm, a country's GDP per capita remains 1% lower than it would have been otherwise.

Transition risk refers to the possibility that companies may get left behind as the world goes green–the industry driven out of business by new regulation, for example, or the technology made obsolete by new advances. Not to mention the brand tarnished by growing activist (and consumer) revolt.

Companies have been aware of these risks for years, in some cases decades, but executives have always seen managing them as a balancing act. Move too quickly and risk leaving behind your core business. Move too slowly and risk getting left behind.

But the swiftness and severity of recent climate events, along with the growing social pressure, have made the biggest companies and investors realize they've been too conservative, leaving them out of step with colossal changes that are already under way. "The degree of capital reallocation and the speed of that is going to be larger and happen more quickly than most market participants expect," Brian Deese, BlackRock's global head of sustainable investing, told TIME in Davos.

Georgieva wants to nudge the system along to make countries and companies acknowledge the threat climate change poses to their bottom lines. For years, the IMF has tested small islands for their exposure; this year it will do the same for Japan, building on pilots done in other advanced economies. At Davos, she endorsed the work central banks are doing to measure how climate change might impact portfolios.

Tackling climate change isn't all bad news for the economy, Georgieva says, as a transition to clean energy sources creates new economic opportunity. "If we really have the courage to move, it may be the silver bullet that boosts the economy," she says.

The newfound urgency of the climate discussion at Davos reflects the reality facing economic leaders. Nonetheless, challenges remain. So far it's mostly just talk, of course. And for all the executives and investors who say they will tackle climate change, there are others who want to squeeze out the last few dollars in the fossil-fuel era. "This is a whole-of-economy transition, and in every sector of the economy there are companies that will be part of the solution and there will be companies that, for whatever reason, lag," Mark Carney, governor of the Bank of England, said at a panel hosted by Bloomberg in Davos.

The companies that have made bold promises still need to deliver on them. As the teenage activist Greta Thunberg said in perhaps her most publicized moment of the week, "Pretty much nothing has been done, since the global emissions of CO[subscript 2] have not reduced." In fact, global temperatures are on track for a rise of 3°C since the Industrial Revolution, even if governments follow through on their current commitments, blowing past the Paris Agreement's target of keeping the temperature rise well below 2°C.

Jennifer Morgan, executive director of Greenpeace International, described the dynamic as a "tension" between companies that see themselves as part of the solution and "an old energy" driving companies that operate with business-as-usual assumptions. A Greenpeace International report released during Davos showed that 24 banks in attendance this year financed the fossil-fuel industry to the tune of $1.4 trillion from the adoption of the Paris Agreement to 2018.

Even as some investors start to step up to change that tide, Georgieva says the transition needs a push from leaders in government, beyond voluntary disclosures of climate risks. "To accelerate progress toward low-carbon, climate-resilient investments, it would be prudent to move toward mandatory disclosure," the Bulgarian said. "It is a welcome sign that some central banks are going in that direction."

For all the ardent declarations of intention at Davos, the true test lies in the months to come. This year will be a critical test of global commitments, as governments prepare to make new pledges to reduce emissions ahead of November's U.N. climate conference in Glasgow. Davos was a good start; leaders are talking. Now they need to act.

In the latest long-term projections, the U.S Energy Information Administration (EIA) projects electricity generation from renewable sources such as wind and solar to surpass nuclear and coal by 2021 and to surpass natural gas in 2045. In the Annual Energy Outlook 2020 (AEO2020) Reference case, the share of renewables in the U.S. electricity generation mix increases from 19% in 2019 to 38% in 2050.

read more

It was another black mark on the privacy record of the social network, which also reported its quarterly earnings.

more @ New York Times

It was another black mark on the privacy record of the social network, which also reported its quarterly earnings.

more @ New York Times

The social network's business has remained robust, even as it grapples with regulatory and competitive pressure.

more @ New York Times

The order formalizes a decision last year to ground the federal agency's drones pending an internal security investigation.

more @ New York Times

The ride-hailing company has faced questions about whether it can make money.

more @ New York Times

As of January 29, 2020 at 09:50PM, 1 BTC equals 9365 USD.

Register PIVOT to get BTC Bonus:PIVOT is a community for cryptocurrency investors.

via free bitcoin

Warren Buffett is getting out of the newspaper business.

Berkshire Hathaway Inc. agreed to sell its BH Media unit and its 30 daily newspapers to Lee Enterprises Inc., which owns papers including the St. Louis Post-Dispatch, for $140 million in cash. Lee has been managing the papers for Buffett's company since 2018, and Berkshire is loaning Lee the money for the purchase.

Buffett, who got a job delivering papers as a teenager and invested in the industry to capitalize on its one-time local advertising stronghold, lamented last year that most newspapers are "toast." BH Media, which owns papers across the country, has been cutting jobs for years to cope with declining ad revenue.

"We had zero interest in selling the group to anyone else for one simple reason: We believe that Lee is best positioned to manage through the industry's challenges," Buffett said in a statement Wednesday.

In 2018, Buffett acknowledged that he was surprised that the decline in demand for newspapers hadn't let up and that his company hadn't found a successful strategy to combat falling advertising and circulation. That same year, U.S. newspaper circulation dropped to its lowest levels since 1940, according to the Pew Research Center.

The Lee sale will include Buffett's hometown Omaha World-Herald and Buffalo News, a paper he's owned for more than four decades, along with 49 weekly publications and a number of other print products, the companies said in the statement. Lee's shares jumped on the news, more than doubling to $2.78 at 9:51 a.m. in New York.

Lee Loan

Berkshire is lending Lee $576 million at a 9% annual rate for the purchase and to refinance other debt. Excluded from the sale is BH Media's real estate, which Lee is leasing under a 10-year agreement.

It's a rare move for the conglomerate as Buffett has long said that he prefers to hold onto businesses. The newspaper deal, however, is Berkshire's second divestiture in less than a year, including the sale of an insurance business in late 2019. Berkshire has held onto other old-fashioned businesses, including door-to-door vacuum-cleaner business Kirby Co. and encyclopedia publisher World Book.

Buffett has longstanding ties to the newspaper industry. He previously owned the Omaha Sun, which won a Pulitzer Prize for its investigation of Boys Town, and struck a deal to buy the World-Herald in 2011. The billionaire investor also had a long friendship with and was a business coach to Katharine Graham, and was a director at her Washington Post Co.

Aside from a few bright spots, such as the largely thriving New York Times Co., the newspaper business is in crisis across the U.S. McClatchy Co. — which owns about 30 newspapers, including the Miami Herald and Charlotte Observer — is fighting to avoid bankruptcy as it contends with pension obligations and debt. The Salt Lake Tribune became a nonprofit last year, after failing to find a profitable business model.

As print advertising has cratered in recent years amid the rise of social media, Craigslist and search ads, private equity firms and hedge funds have swooped in to take advantage of newspapers' steady though dwindling revenue streams.

New Media Investment Group Inc., controlled by private equity firm Fortress Investment Group LLC, bought USA Today owner Gannett Co. last year to form the largest U.S. newspaper chain. The deal spurred apprehension in journalism circles given New Media's reputation for newsroom layoffs, though the new Gannett leadership pledged to avoid widespread job cuts.

––With assistance from Gerry Smith.

The dollars are adding up fast. So here are some tips for pruning the subscriptions you no longer use.

more @ New York Times

The U.S. Energy Information Administration (EIA) will release updated projections of future U.S. energy production and use in its Annual Energy Outlook 2020 (AEO2020) today at 11:00 a.m. ET. The AEO2020 Reference case, which serves as a baseline for exploring the effects of different assumptions about the economy, policy, and technology, projects renewables to be the fastest-growing source of electricity generation through 2050, driven by continued declines in the capital costs for solar and wind technologies. Slow growth in U.S. energy consumption, as a result of continued increases in energy efficiency, and technologically enabled growth in domestic oil and natural gas production lead the United States to remain a net energy exporter through 2050.

read more

At a facility near Berlin, a new kind of robot is automating tasks that until recently had been out of the reach of machines.

more @ New York Times

Apple found renewed growth with an increase in phone sales as well as younger products, like the Apple Watch, AirPods and its subscription services.

more @ New York Times

The police hoped that taking down online black markets would chase away criminals. But the amount of Bitcoin spent on illegal purposes has reached a new high.

more @ New York Times

As of January 28, 2020 at 09:50PM, 1 BTC equals 9038.0996 USD.

Register PIVOT to get BTC Bonus:PIVOT is a community for cryptocurrency investors.

via free bitcoin

Astronomers using data from NASA's Chandra X-ray Observatory and other telescopes have put together a detailed map of a rare collision between four galaxy clusters.

January 28, 2020

The U.S. government spending bill signed into law in late December 2019 included several provisions related to federal energy programs. Among these provisions was the reinstatement of a $1.00 per gallon biodiesel mixture credit, commonly referred to as the biodiesel tax credit (BTC). The BTC applies to both biodiesel and renewable diesel (referred to as biomass-based diesel) through 2022. The credit was also retroactively applied to 2018 and 2019.

read more

The move points up how an American effort against the Chinese wireless equipment company has stumbled.

more @ New York Times

(BOSTON) — Chipotle was hit with a $1.3 million fine over more than 13,000 child labor violations at its Massachusetts restaurants, the state's attorney general announced Monday.

Attorney General Maura Healey ordered the largest child labor penalty ever issued by the state against the Mexican restaurant chain after finding an estimated 13,253 child labor violations in its more than 50 locations.

"Chipotle is a major national restaurant chain that employs thousands of young people across the country and it has a duty to ensure minors are safe working in its restaurants," Healey said in a statement. "We hope these citations send a message to other fast food chains and restaurants that they cannot violate our child labor laws and put young people at risk."

The fine detailed that Chipotle had employees under the age of 18 working past midnight and for more than 48 hours a week. Teenagers told investigators their hours of work were so long that it was preventing them from keeping up with their schoolwork. The company also regularly hired minors without work permits.

The settlement total is closer to $2 million, including penalties for earned sick time violations in which managers granted employees paid time off only for certain illnesses. The violations also include failure to keep accurate records and pay timely wages. Lastly, the company was ordered a voluntary $500,000 payout to a state youth worker fund dedicated to education, enforcement and training.

Spitzer Space Telescope, one of agency's great observatories, one of Spitzer's great discoveries was that of the TRAPPIST-1 star, an ultra-cool dwarf, which has seven Earth-size planets orbiting it.

January 27, 2020

As of January 27, 2020 at 09:50PM, 1 BTC equals 8658.0098 USD.

Register PIVOT to get BTC Bonus:PIVOT is a community for cryptocurrency investors.

via free bitcoin

The sheer volume of criticism of the government, and the sometimes clever ways that critics dodge censors, are testing Beijing's ability to control the narrative.

more @ New York Times

In the January 2020 update of its Short-Term Energy Outlook (STEO), the U.S. Energy Information Administration (EIA) forecasts that U.S. crude oil production will average 13.3 million barrels per day (b/d) in 2020, a 9% increase from 2019 production levels, and 13.7 million b/d in 2021, a 3% increase from 2020.

read more

Byte, a new video-sharing app released Friday to compete with ByteDance's TikTok, has rocketed to the top of Apple's U.S. App Store.

Created by Dom Hofmann, Byte reboots the deprecated Vine video-sharing service, which he co-founded in the summer of 2012 and sold to Twitter later that year. The parent company failed to find a way to make the service profitable and eventually discontinued it in 2016. Despite its brief existence, Vine became a cultural touchpoint in the U.S., with many users embracing its six-second time limit as a creative challenge. It was where controversial YouTube star Logan Paul, whose channel now has more than 20 million subscribers, got his start.

Byte "ended Friday as the No. 1 free iPhone app on the U.S. App Store and is still in the top spot," said Randy Nelson of research firm Sensor Tower. Beside the U.S., Byte is also the top free iOS app in Canada and ranks in the top 10 in Australia, New Zealand, Norway and the U.K. On Android's Play Store, Byte is sixth among free apps in the U.S.

The timing of Byte's release coincides with a moment of reckoning for TikTok and its Beijing-based parent company. ByteDance is looking to hire a chief executive officer for TikTok, which is under increasing scrutiny from U.S. lawmakers wary about the influence of Chinese companies on American consumers. TikTok's runaway popularity has been deemed to create "national security risks," according to a letter by Senators Chuck Schumer and Tom Cotton in the fall.

Unlike ByteDance, which is the world's highest-valued startup, and most other social media contenders, Byte is starting off small and its community guidelines make several references to the company's modest budget. Still, the strong early response to Byte's arrival — coming with little to no advance fanfare — suggests the community that Vine built up remains loyal to the particular six-second format. Some of the early popular videos on the platform are humorous proclamations of "Don't post TikToks here."

As of January 26, 2020 at 09:50PM, 1 BTC equals 8384.8496 USD.

Register PIVOT to get BTC Bonus:PIVOT is a community for cryptocurrency investors.

via free bitcoin

As of January 25, 2020 at 09:50PM, 1 BTC equals 8312.2197 USD.

Register PIVOT to get BTC Bonus:PIVOT is a community for cryptocurrency investors.

via free bitcoin

Reporting about the powerful tool with a database of three billion photos "troubled" the state's attorney general, who asked for an inquiry into its use.

more @ New York Times

The tech giant has begun charging U.S. law enforcement for responses to search warrants and subpoenas.

more @ New York Times

As of January 24, 2020 at 09:50PM, 1 BTC equals 8339.0498 USD.

Register PIVOT to get BTC Bonus:PIVOT is a community for cryptocurrency investors.

via free bitcoin

All eyes are on south Mississippi with this month's delivery and installation of NASA's Space Launch System.

January 24, 2020

An analysis of a phone belonging to Jeff Bezos found malicious code was hidden in a video sent from a WhatsApp account belonging to Crown Prince Mohammed bin Salman.

more @ New York Times

U.S. oil production from tight formations increased in 2019, accounting for 64% of total U.S. crude oil production. This share grew because of the increasing productivity of new wells that were brought online during 2019. Since 2007, the average first full month of oil production from new wells in regions tracked by the U.S. Energy Information Administration's (EIA) Drilling Productivity Report (DPR) has increased. The growing initial production rates have helped oil production from tight formations to increase despite the slowdowns in drilling activity when oil prices fell between 2015 and 2016. Since 2017, recovering oil prices and more efficient production from new wells have helped producers cover costs of drilling, production, and the development of new technologies.

read more

Just a year ago, the world's richest man seemed to have a pretty low-key life. Times sure have changed.

more @ New York Times

The story of automation in America has long been told in shuttered factories and declining Midwestern cities. But the latest wave of advancements in artificial intelligence may be bring the prospect of machine replacement beyond blue collar work. Developers are creating algorithms that promise to take over vast amounts of work in white collar fields like law and medicine, potentially upending traditionally high-status fields. For people in those once-secure positions, the questions are whose jobs may be changed, how soon, and what new opportunities may arise to take their place.

Knowledge work that involves repetitive tasks or large amounts of data, such as lawyers' often arduous document discovery process, is particularly ripe for disruption from AI, experts say. Tasks that require human-to-human interaction or some element of creativity are likely to be safer. "Pattern recognition in general is something that these technologies seem good at," says Mark Muro, one of the authors of a recent Brookings Institution report that suggests high-paid, educated workers will be highly exposed to new AI technology. "That is a contribution to a lot of white collar activities."

MIT economics professor David Autor says middle management positions are particularly susceptible to this new wave of automation, particularly in fields like finance and inventory management, where humans are in charge of translating data into concrete business decisions. But he also argues that displacement from machine learning is likely to create new opportunities.

"Historically, tons of new work comes into existence as a result of automation," Autor says. "The whole industrial revolution came about as a result of the automation of artisanal tasks, but it would have been impossible for anyone at the dawn of that period to foresee where that would go."

That optimism may come as cold comfort for the artisans of 2020: the millions of paralegals, human resource managers, IT professionals and other knowledge industry workers whose positions are prime targets for a new wave of automation. McKinsey predicts across-the-board cuts in such fields over the next decade. Some fields, like office financial support personnel, are likely to lose more than one in four positions.

Some economists predict even more dramatic changes in the coming years, including a radical shift in top-tier white collar work. Richard Baldwin of the Graduate Institute in Geneva argues that AI, coupled with outsourcing enabled by new advances in telecommunications, will sharply reduce white collar employment. He believes those twin drivers could displace professionals in elite sectors from media and finance to architecture and law, at least until people find new ways to put themselves to work.

"What we have is displacement being driven at the pace of digital technology, but job creation being driven at the pace of human ingenuity," Baldwin says. "What I'm worried about is that job displacement driven by digital will outstrip job creation driven by ingenuity."

Recent advancements illustrate the extent of possible change in some of society's most illustrious professions. This month, a team of researchers announced they had created an AI algorithm that outperformed radiologists in detecting breast cancer in mammograms. Trained on tens of thousands of mammogram images, the algorithm measurably reduced both false positives and false negatives compared to human doctors. Of course, radiology involves a lot more than classifying images. With demand for radiologists surging, it's not likely the field will die off any time soon. "AI will not replace radiologists," says Kevin Lyman, CEO of AI radiology startup Enlitic. "But radiologists using AI will replace those who do not."

Of course, there are winners in any mass economic reorientation. The explosion in AI development has already created thousands of high-paying jobs for those with the skill sets to design, test, and sell such systems. Hiring growth for "AI Specialists" grew by 74% annually over the past four years, according to LinkedIn data. Carnegie Mellon University, a premier school for computer science, reports a recent explosion of interest in hiring their graduates, with three times as many tech companies recruiting in 2019 compared to just three years earlier. Over the same period, the number of data analytics, information technology, and software engineering jobs posted to CMU's recruitment portal also tripled.

Even within the tech campuses of Silicon Valley, machine learning automation may be making inroads. San Francisco-based startup Kite has developed a plugin that uses AI to offer auto-complete suggestions for coders. CEO and Founder Adam Smith predicts the technology will eventually do much more. "Instead of Kite predicting the line of code you're currently typing, the human will just tell us what they want the piece of code to do and we'll synthesize that code for them," says Smith. But while coders may be working faster, he maintains that the obsolescence of software engineers is a long way off.

Even as some high-status professions face possible AI disruption, economists are generally optimistic about the future of employment. Few are predicting anything like the end of work as we know it in coming decades. The challenge, says Erik Brynjolfsson, a professor of management science and information technology at MIT, is finding ways to transition people away from work where machines are outpacing humans and into jobs where they will be most needed.

"In healthcare, in childcare, cleaning the environment, in creative work, science, entrepreneurship, the arts — these are all areas where machines can't hold a candle to humans," he says. "We've got plenty of work for people to do."

As of January 23, 2020 at 09:50PM, 1 BTC equals 8583.7598 USD.

Register PIVOT to get BTC Bonus:PIVOT is a community for cryptocurrency investors.

via free bitcoin

In its Short-Term Energy Outlook (STEO), released on January 14, the U.S. Energy Information Administration (EIA) forecasts that U.S. natural gas exports will exceed natural gas imports by an average 7.3 billion cubic feet per day (Bcf/d) in 2020 (2.0 Bcf/d higher than in 2019) and 8.9 Bcf/d in 2021. Growth in U.S. net exports is led primarily by increases in liquefied natural gas (LNG) exports and pipeline exports to Mexico. Net natural gas exports more than doubled in 2019, compared with 2018, and EIA expects that they will almost double again by 2021 from 2019 levels.

read more

Online forums carry personal details of potential targets like industry leaders and their families. The police are struggling to find a solution.

more @ New York Times

Twitter said Clearview AI, whose app is spreading in law enforcement, was violating its policies. Lawmakers also expressed privacy concerns.

more @ New York Times

It most likely began with a tiny bit of code that implanted malware, which gave attackers access to Mr. Bezos' photos and texts.

more @ New York Times

As of January 22, 2020 at 09:50PM, 1 BTC equals 8732.0303 USD.

Register PIVOT to get BTC Bonus:PIVOT is a community for cryptocurrency investors.

via free bitcoin

The Amidon-Bowen Elementary School choir performs at the MLK Day of Service.

January 22, 2020

Voice-activated helpers can automate life's little chores, once you get the hang of them.

more @ New York Times

According to the U.S. Energy Information Administrationâs (EIA) International Energy Outlook 2019 (IEO2019), global electric power generation from renewable sources will increase more than 20% throughout the projection period (2018â"2050), providing almost half of the worldâs electricity generation in 2050. In that same period, global coal-fired generation will decrease 13%, representing only 22% of the generation mix in 2050. EIA projects that worldwide electricity generation will grow by 1.8% per year through 2050.

read more

The futuristic Origin, which seats six passengers and lacks a steering wheel, will require intensive testing and regulatory scrutiny before it can hit the streets.

more @ New York Times

Two United Nations experts plan to release a public statement Wednesday morning "addressing serious allegations."

more @ New York Times

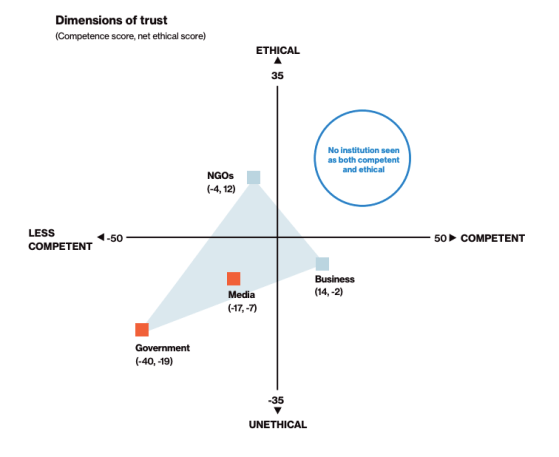

A new report found widespread distrust in societal institutions — defined as government, business, NGOs and the media — despite a strong global economy, a phenomenon it deemed a "trust paradox." The report concluded that people's fears about the future are driving this trend, and proposed institutions prioritize balancing competence with ethical behavior to rebuild public trust.

The "Trust Barometer 2020" report was conducted by the communications firm Edelman, which has been running the survey for the past 20 years. The Barometer, which aims to survey trust and credibility around the world, is usually released at the start the World Economic Forum in Davos, Switzerland, which began on Tuesday. The 2020 barometer surveyed over 34,000 people in 28 countries.

Despite the strong global economy, the report found that 56% of respondents believe capitalism as it exists today does more harm than good in the world; fewer than one in three people in developed markets said they believe they and their families will be better off in five years. The report found that, globally, 83% of employees are worried about losing their jobs to reasons including automation, a looming recession, lack of training, cheaper foreign competition, immigration and the gig economy.

"We are living in a trust paradox," said Richard Edelman, Edelman CEO, in a statement. "Since we began measuring trust 20 years ago, economic growth has fostered rising trust. This continues in Asia and the Middle East but not in developed markets, where national income inequality is now the more important factor. Fears are stifling hope, and long-held assumptions about hard work leading to upward mobility are now invalid."

The Barometer found that none of the four institutions it asked about — government, business, NGOs and the media — are trusted. Wealthier, more educated individuals trusted institutions more than the rest of the population, a gap it describes as the "mass-class" trust divide. The report found that this divide reached record levels in a record number of countries.

The survey also found that trust in technology companies has substantially declined, with a global four point decline in trust in the technology sector from 2019 to 2020 and substantial declines of 10 points in France, eight points in Canada, Italy, Russia and Singapore, and seven points in the U.S. Sixty one percent of people responded that they felt the pace of change in technology is too fast, and 66% responded that they "worry technology will make it impossible to know if what people are seeing or hearing is real."

In a similar vein, respondents worried about receiving accurate information. Fifty seven percent agreed that the media they consume is "contaminated with untrustworthy information" and 76% of people said they worry about "fake news being used as a weapon" — a six-point increase from 2018.

There's also a lack of faith that the government can address these problems. Sixty six percent of respondents said they do not have confidence that "our current leaders will be able to successfully address our country's challenges."

Just 46% people said they trust religious leaders, 42% said they trust government leaders and 36% said they trust the very wealthy. On a more positive note, 80% of respondents said they trust scientists, 69% said they trust "people in my local community" and 65% said they trust "citizens of my country."

Competence versus ethical behavior

"People's expectations of institutions have led us to evolve our model for measuring trust," said Edelman. "Trust today is granted on two distinct attributes: competence (delivering on promises) and ethical behavior (doing the right thing and working to improve society). It is no longer only a matter of what you do—it's also how you do it."

Significantly, the Barometer found that no institutions were viewed as both competent and ethical. Business was seen as competent and NGOs were seen as ethical, while the government and the media were seen as neither.

The report found that people are three times as likely to trust a company if they think it acts ethically, rather than just competently. It also found that employees expect their employers to act ethically, with 92% of employees said it is important for their their employer's CEO to "speak out" on issues like income inequality, diversity, ethical use of tech, climate change and immigration.

"After tracking 40 global companies over the past year through our Edelman Trust Management framework we've learned that ethical drivers such as integrity, dependability and purpose drive close to 76 percent of the trust capital of business, while competence accounts for only 24 percent," said Antoine Harary, president of Edelman Intelligence. "Trust is undeniably linked to doing what is right. The battle for trust will be fought on the field of ethical behavior."

As of January 21, 2020 at 10:50PM, 1 BTC equals 8638.0898 USD.

Register PIVOT to get BTC Bonus:PIVOT is a community for cryptocurrency investors.

via free bitcoin

SmileDirectClub, which sells teeth aligners online, has worked to limit information about customer dissatisfaction.

more @ New York Times

SpaceX's Falcon 9 rocket lifts off from Launch Complex 39A at the Kennedy Space Center at 10:30 a.m. EST on Jan. 19, 2020.

January 21, 2020

In the U.S. Energy Information Administration's (EIA) January Short-Term Energy Outlook (STEO), EIA forecasts that the Brent crude oil spot price will average $65 per barrel (b) in 2020 and $68/b in 2021 and that the West Texas Intermediate (WTI) spot price will average $59/b in 2020 and $62/b in 2021.

read more

The ride-hailing giant agreed to sell Uber Eats in India to rival Zomato, continuing its recent efforts to exit money-losing businesses.

more @ New York Times

As of January 20, 2020 at 09:50PM, 1 BTC equals 8676.2598 USD.

Register PIVOT to get BTC Bonus:PIVOT is a community for cryptocurrency investors.

via free bitcoin

I reported on an app, created by the company Clearview AI, that can identify people in seconds using a trove of photos collected from across the web.

more @ New York Times

A new report found that the world's 2,153 billionaires have more wealth than 4.6 billion people, underscoring the degree of global inequality.

The Oxfam International study, released Monday and dubbed "Time to Care," shows that the number of billionaires has doubled in the past decade. The authors add that these fortunes have largely been amassed while everyday people, especially poor women, continue to struggle.

"The gap between rich and poor can't be resolved without deliberate inequality-busting policies, and too few governments are committed to these," Oxfam India CEO Amitabh Behar said in a press statement. "Our broken economies are lining the pockets of billionaires and big business at the expense of ordinary men and women. No wonder people are starting to question whether billionaires should even exist."

The report finds that women are most impacted by the growing equality gap — the 22 richest men in the world have more money than all the women in Africa, for example. Also, 12.5 billion hours of unpaid care work is done by women and girls every day, which contributes $10.8 trillion dollars a year to the global economy, the report found. Women also do more than three-quarters of all unpaid care work and make up two-thirds of the paid 'care workforce," Oxfam said.

Governments are not taxing the wealthiest people or corporations enough, the report argues. Oxfam found that if the world's richest one percent had to pay an extra 0.5 in taxes over the next 10 years, that would be equal to the investment that is needed to add over 100 million jobs in workforces like health, education and childcare.

"Governments must prioritize care as being as important as all other sectors in order to build more human economies that work for everyone, not just a fortunate few," Behar said.

Like Trump, India is pressuring both of Mr. Bezos' businesses as its leaders become more nationalistic toward foreign companies and news media.

more @ New York Times

I reported on an app, created by the company Clearview AI, that can identify people in seconds using a trove of photos collected from across the web.

more @ New York Times

As of January 19, 2020 at 09:50PM, 1 BTC equals 9064.9902 USD.

Register PIVOT to get BTC Bonus:PIVOT is a community for cryptocurrency investors.

via free bitcoin

Former White House Chief Economic Advisor Gary Cohn said Sunday that President Trump's tariffs on steel and aluminum "hurt the U.S." and did not help the administration in trade negotiations, either.

"I don't think the tariffs helped us get to any different outcome. I think it has hurt the U.S. It's totally hurt the United States," Cohn said on CBS's Face the Nation.

Cohen stated in response to CBS host Margaret Brennan's that he didn't believe the tariffs changed the U.S.' progress on the U.S.-Mexico-Canada agreement or trade negotiations with China.

Cohn also acknowledged his differing stance on trade negotiations to Trump, saying that they "agreed fundamentally on what the issue was" but not how to solve it. Still, he denied that their disagreement on tariffs and trade were the only reason he left the administration in March of 2018. "I left the administration for a variety of different reasons," Cohn said.

"The US economy is very strong, very solid. Employment growth is great but we're missing a big component," Cohn said. "We're missing the capital expenditures from companies in the United States."

As of January 18, 2020 at 09:50PM, 1 BTC equals 8869.1904 USD.

Register PIVOT to get BTC Bonus:PIVOT is a community for cryptocurrency investors.

via free bitcoin

(WASHINGTON) — The Trump administration has granted Chevron a special license to keep drilling oil in Venezuela despite a ban on American companies doing business with President Nicolás Maduro's socialist government.

The Treasury Department late Friday renewed until April 22 the license for Chevron and four other U.S. service suppliers that are among the last American companies operating in the oil-rich South American nation. It's the fourth time the U.S. has exempted the companies from the Venezuela ban.

Chevron, a San Ramon, California-based company, has operated in Venezuela for almost a century. Its four joint ventures with Venezuela's state-run oil monopoly PDVSA produce about 200,000 barrels a day. That's about a quarter of Venezuela's total production, according to the Organization of the Petroleum Exporting Countries.

Critics among Venezuela's opposition insist that Chevron's continued presence in the country undercuts the Trump administration's goal of ousting Maduro by providing him a valuable lifeline of badly-needed export dollars.

A little-known start-up helps law enforcement match photos of unknown people to their online images — and "might lead to a dystopian future or something," a backer says.

more @ New York Times

Until Friday, few executives had complained in public about how Google, Apple, Amazon and Facebook hurt their businesses.

more @ New York Times

A growing number of academics are challenging assumptions about the negative effects of social media and smartphones on children.

more @ New York Times

As of January 17, 2020 at 09:50PM, 1 BTC equals 8896.1104 USD.

Register PIVOT to get BTC Bonus:PIVOT is a community for cryptocurrency investors.

via free bitcoin

This bright, somewhat blob-like object — seen in this image taken by the NASA/ESA Hubble Space Telescope — is a galaxy named NGC 1803. It is about 200 million light-years away, in the southern constellation of Pictor (the Painter's Easel), and it was discovered in 1834 by astronomer John Herschel.

January 17, 2020

There are tools to crack into the phones at the center of a new dispute over encryption. But the F.BI. says it still needs Apple's aide.

more @ New York Times

There are tools to crack into the phones at the center of a new dispute over encryption. But the F.BI. says it still needs Apple's aide.

more @ New York Times

In its latest Short-Term Energy Outlook (STEO), released on January 14, the U.S. Energy Information Administration (EIA) forecasts year-over-year decreases in energy-related carbon dioxide (CO2) emissions through 2021. After decreasing by 2.1% in 2019, energy-related CO2 emissions will decrease by 2.0% in 2020 and again by 1.5% in 2021 for a third consecutive year of declines.

read more

(Bloomberg) — Comcast Corp.'s NBCUniversal said its upcoming streaming service will be free to everyone — with extra programming for its pay-TV subscribers — in a bet that it can generate substantial revenue from advertising while supporting the cable business.

Along with AT&T Inc.'s HBO Max, NBC's new service, Peacock, is poised to be a relatively late entrant in the burgeoning market for streaming-video services. But Peacock also marks a very different approach from rivals. Unlike paid-subscription platforms such as Netflix Inc., Walt Disney Co.'s Disney+ and Apple Inc.'s Apple TV+, Peacock will largely rely on advertising. The company expects to reach 30 million to 35 million active accounts by 2024.

Comcast executives have said they plan to spend $2 billion over the next two years on the streaming service and expect it to break even by its fifth year. The approach mimics the deep spending of rivals such as Disney and AT&T, which are pouring billions into their platforms as well — and don't expect to be profitable until later in the decade.

The Peacock service, named for the longstanding NBC logo, will launch April 15 to Comcast customers and then roll out nationwide July 15. That's just before the start of the Summer Olympics, which NBCUniversal's networks will air. The premium version of Peacock, which ordinarily will cost $4.99 a month, will be available at no cost initially to subscribers of Comcast and Cox Communications Inc.

Those two cable companies have over 24 million subscribers. Their subscribers will have access to twice as many hours of content as those using the free version. That will include sports offerings like soccer's English Premier League and early access to late-night talk shows.

Ad Options

Anyone can get the free version of Peacock, but customers will have to pay $4.99 for the premium version with advertising. They can also pay $9.99 for an advertising-free version.

By making a version of the product free, NBC is hoping that Peacock will have a leg up on its streaming competitors and reach a large subscriber base quickly. It also reflects the fact that Peacock is owned by Comcast, the largest U.S. cable-TV provider, which can use a free streaming service to make its other offerings more attractive.

State Farm Life Insurance Co., Target Corp. and Unilever will be the first set of advertisers on Peacock.

The service will have programming from the Summer Olympics, which begin in late July in Tokyo, including live coverage of the opening and closing ceremonies and daily Olympic shows.

Peacock will have more than 600 movies and 400 series, including reruns of NBC shows such as "The Office" and "Parks and Recreation," as well as a slate of original programs. It will also stream the "Law & Order" and "Chicago" shows created by Dick Wolf and have exclusive streaming rights for Universal films, including "Fast & Furious 9" and "Jurassic World 3."

The arrival of Peacock comes during a period of transition for NBCUniversal. Steve Burke stepped down as the chief executive officer on Jan. 1, handing the reins to lieutenant Jeff Shell. Burke, who is now chairman of NBCUniversal, will retire in August.

Going into 2020, the U.S. economy generally seems strong — especially for women, who hold the majority of jobs for the first time in almost a decade. Women held 50.04% of American jobs as of December, excluding farm workers and the self-employed, according to the Bureau of Labor Statistics. That's up from 49.7% just one year ago.

What's driving the surge in female employment? The two industries that experienced the biggest overall gains, health care and retail, both employ many women and are fueled in part by demand from economically-empowered female consumers, says Amanda Weinstein, assistant professor of economics at the University of Akron.

Meanwhile, as women have gained increased control of spending in American households and entered the workforce over the last century, they've helped fuel the rise of the service sector, which includes healthcare, education and retail, all industries with lots of female employment. In turn, services such as daycare, home health care, and food preparation have made it easier for women to join the workforce.

But economists say that this isn't the entire story, and forces in the workplace and society more broadly are still holding many women (and men) back. Here are three things to know about women in the workforce:

Employed, but with low pay

Many women are working in the service sector, which includes plenty of high-paying professions, like physicians. But Aparna Mathur, the director of the American Enterprise Institute-Brookings Paid Family Leave Project, says that many of this sector's low-paying jobs, such as home health aides, are predominantly held by women.

Indeed, Mathur says that simply holding a job doesn't necessarily ensure financial security. While health care costs have risen and there is high demand for workers to care for the aging population, wages for low-paid healthcare workers haven't risen significantly. That's due in part to the supply of immigrant workers and a high turnover rate. "These are not long-term careers for a lot of people, so it's hard to imagine that this would suddenly lead to higher wages for workers in these industries," Mathur says.

Some economists argue that workers who oversee or care for others, such as teachers and home health aides, are underpaid relative to their societal importance because what they do is viewed as "care work."

"Historically, we have undervalued care work because it has been seen as very feminine. And we tend to undervalue feminine jobs that involve care," Weinstein says.

The childcare conundrum

The high number of women in the workforce conceals the facts that the labor force participation rate for many groups of women is still lower than that of men. (The civilian workforce participation rate for prime age workers (ages 25 to 54) was 76.8% for women in Dec. 2019 compared to 89.2% for men.) Meanwhile, women are much more likely to work part time.

Mathur says there's evidence that more women have been forced to choose more flexible work, which may be part time and closer to home, because they need or are expected to provide care for their families. In part, this may be due to the high cost of childcare. More than 70% of families spend more than 10% of their incomes on care, according to analysis by Care.com.

"We've had a decade where women were underemployed relative to men," says Mathur.

Policies that help families ensure that care is available at home, such as a federal paid leave program, could free up more women to join the workforce, Mathur says.

Weinstein says that reevaluating conventions in the workplace and at American schools could also help women. For instance, the 9 a.m. to 4 p.m. school day and lengthy summer vacations from school may not make sense with two parents working full time.

"We have a society that, in many ways, has not pivoted to support the workforce that we currently have. And we have dual earners," says Weinstein.

Some men are struggling, too

The increasing proportion of female workers leaves a big unanswered question: what's happening to the men?

Male participation in the workforce has been generally declining for decades. Although there was an increase in 2019, only 89.2% of men ages 25 to 54 were in the workforce last December, compared to 97.1% in Dec. 1960.

Claudia Goldin, a professor of economics at Harvard University, says that women are reaping the benefits of being more educated than men. However, workforce participation has declined even for men with college degrees. Part of the problem, she says, is that the changing economy is leaving some men behind.

"Some men are not as employable in the old sectors, and they're not doing a very good job of moving into the new sectors. This is certainly true about the college-educated population," says Goldin.

In Weinstein's view, the same stigma that has devalued care work has also discouraged men from pursuing traditionally female professions, even if there are more opportunities there.

"We are starting to see men join some of those jobs, but not at the rate we're seeing women join male-dominated sectors. Not nearly the rate," says Weinstein.

Mathur says that men may be struggling to remain in the workforce for many other reasons — including the opiate epidemic and criminal records — and that more research is necessary to determine what's happening.

"We need to understand better what is driving the decline," says Mathur. "We look at issues like the opioid crisis, the incarceration rate, is it disability? I think with men, some of these issues will be handled with a tighter labor market. So we are already seeing employers reaching out to demographics they typically haven't wanted to employ, [such as] people who have a criminal record."

The internet search giant became the fourth tech company — after Apple, Amazon and Microsoft — to reach the market milestone.

more @ New York Times

As of January 16, 2020 at 09:50PM, 1 BTC equals 8696.7197 USD.

Register PIVOT to get BTC Bonus:PIVOT is a community for cryptocurrency investors.

via free bitcoin

The pilots of a Delta flight conducting an emergency landing didn't tell air traffic controllers before dumping fuel that wound up falling on several Los Angeles area schools on Tuesday, aviation officials said Thursday.

"A review of yesterday's air traffic control communications shows the Delta Flight 89 crew did not tell air traffic control that they needed to dump fuel," the Federal Aviation Administration (FAA) said in a statement emailed to TIME.

Pilots typically notify flight controllers if they believe they need to dump fuel, a procedure that is sometimes done to reduce an aircraft's weight ahead of an emergency landing for safety reasons.

According to a recording of the conversation between a Flight 89 pilot and an air traffic controller from LiveATC.net and reported by CNN, a pilot explicitly said he or she did not need to dump fuel:

Tower: "OK, so you don't need to hold or dump fuel or anything like that?"

Pilot: "Uh, negative."

Furthermore, the pilots did not dump fuel "at an optimal altitude" that would have allowed the fuel to dissipate before it reached the ground, the FAA said.

If circumstances allow, controllers can direct pilots in need of a fuel dump to an area where it's safer to perform the maneuver. However, in an emergency situation, it is ultimately up to pilots to do what they believe is necessary for the safety of their aircraft and those aboard. Whether the fuel dump in Tuesday's situation was warranted given the aircraft's situation and position will be central to the investigation of the incident.

Delta Air Lines refused to comment, citing the ongoing investigation. A Delta spokesperson previously said that the aircraft "landed safely after a release of fuel, which was required as part of normal procedure to reach a safe landing weight."

Delta Air Lines Flight 89 had been en route from Los Angeles to Shanghai and landed just 15 minutes after takeoff on Tuesday at 11:47 a.m., Los Angeles International Airport officials had said.

Fuel dumped by the aircraft fell across five elementary schools and one high school and fire crews treated 60 people for minor injuries, officials said, according to CNN.

No one was hospitalized as a result of the incident. "Students and staff were on the playground at the time and may have been sprayed by fuel or inhaled fumes," a Los Angeles Unified School District spokesperson said in an earlier statement.

NYT Technology: How to Fight Health ‘Cures’ Online

NASA Image of the Day: Perseverance Rover Mated to...

NYT Technology: Massachusetts Sues Uber and Lyft O...

U.S. crude oil and natural gas production in April...

Air Force says service still needs to be bigger - ...

Facebook reportedly considers ban on political ads...

1 BTC equals 9310.0801 USD

NYT Technology: YouTube’s Factory Workers Are Angry

NASA Image of the Day: Hubble Sees a Star Called H...

April 2006

May 2006

June 2006

July 2006

August 2006

September 2006

October 2006

November 2006

December 2006

February 2007

April 2007

May 2007

June 2007

July 2007

August 2007

September 2007

October 2007

November 2007

December 2007

January 2008

February 2008

April 2008

May 2008

July 2008

August 2008

September 2008

October 2008

November 2008

January 2009

May 2009

June 2009

July 2009

August 2009

September 2009

December 2009

March 2010

June 2010

July 2010

September 2010

October 2010

November 2010

January 2011

March 2011

February 2013

April 2013

September 2013

December 2013

August 2014

September 2014

October 2014

November 2014

January 2015

January 2016

September 2018

October 2018

November 2018

December 2018

January 2019

February 2019

March 2019

April 2019

May 2019

June 2019

July 2019

August 2019

September 2019

October 2019

November 2019

December 2019

January 2020

February 2020

March 2020

April 2020

May 2020

June 2020

July 2020